Advice for Living Through These Uncertain Times

Joe Tomkins • May 27, 2020

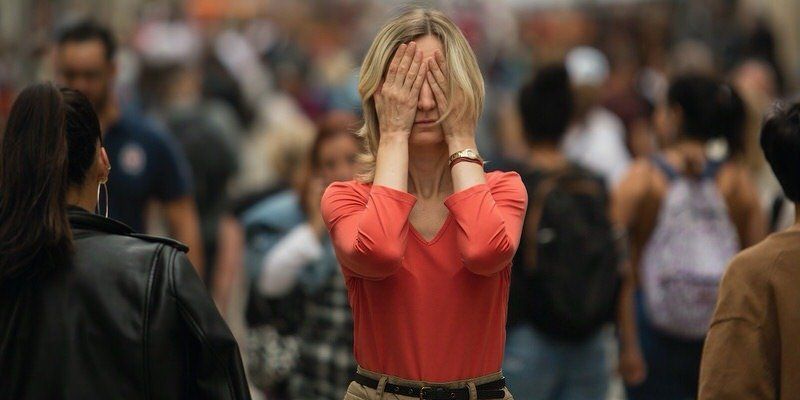

It only takes a quick trip to the grocery store to realize that life is VERY different than it was just a couple of months ago. COVID-19 has already left a permanent mark in modern human history. So as you continue life mid-pandemic, here's some good advice: don’t believe everything you read on the internet or see in the news.

As it relates to your personal financial situation.

As it relates to the Canadian economy.

As it relates to the value of your home.

As it relates to Canadian real estate values.

Because as the media continues to cover COVID-19, you can expect to see financial doomsday headlines; designed to grab your attention, get more outlandish as time goes on. The goal is to catch your eye with a wild headline so that you read an article (or watch a video) and are exposed to the advertisements contained within.

Media and news companies are in the business of selling advertisements, not providing you with accurate unbiased information.

The best way to grab your attention is with an attempt to instil fear or shock. One headline will read that house prices are expected to plummet, the next will claim mortgage defaults are on the rise by a billion per cent, while the next will provide incredible proof that house sales are expected to grind to a screeching halt and will never return to normal.

And although most of these stories contain *some* level of truth, rest assured that what may be true for the rest of Canada (or the US) is not necessarily true about your personal financial situation, your local economy, your local real estate, or your mortgage.

Don’t buy into the hype and get anxious about things you can’t control.

It might be best to just turn off the TV, put down the newspaper, and stop scrolling Facebook. Especially if you aren't thinking of making a move anytime soon anyway! But if your mortgage is up for renewal, if you're thinking of buying a new property, or if you're looking to make a change with your investments, then it's best to talk with local professional and seek their advice!

Be influenced by those who have your best interest in mind!

If you have any questions about your mortgage, please don’t hesitate to contact me anytime. I’d be more than happy to let you know exactly where you stand.

Thinking of Calling Your Bank for a Mortgage? Read This First. If you're buying a home or renewing your mortgage, your first instinct might be to call your bank. It's familiar. It's easy. But it might also cost you more than you realize—in money, flexibility, and long-term satisfaction. Before you sign anything, here are four things your bank won’t tell you—and four reasons why working with an independent mortgage professional is the smarter move. 1. Your Bank Offers Limited Mortgage Options Banks can only offer what they sell. So if your financial situation doesn’t fit neatly into their guidelines—or if you’re looking for competitive terms—you might be out of luck. Working with a mortgage broker? You get access to mortgage products from hundreds of lenders : major banks, credit unions, monoline lenders, alternative lenders, B lenders, and even private funds. That means more options, more flexibility, and a much better chance of finding a mortgage that fits you. 2. Bank Reps Are Salespeople—Not Mortgage Strategists Let’s be honest: most bank mortgage reps are trained to sell their employer’s products—not to analyze your financial goals or tailor a long-term mortgage plan. Their job is to generate revenue for the bank. Independent mortgage professionals are different. We’re not tied to one lender—we’re tied to you. Our job is to shop around, negotiate on your behalf, and recommend the mortgage that offers the best balance of rate, terms, and flexibility. And yes, we get paid by the lender—but only after we find you a mortgage that works for your situation. That creates a win-win-win: you get the best deal, we earn our fee, and the lender earns your business. 3. Banks Don’t Lead with Their Best Rate It’s true. Banks often reserve their best rates for those who ask for them—or threaten to walk. And guess what? Most people don’t. Over 50% of Canadians accept the first renewal offer they get by mail. No questions asked. That’s exactly what the banks count on. Mortgage professionals don’t play that game. We start by finding lenders offering competitive rates upfront, and we handle the negotiations for you. There’s no guesswork, no pressure, and no settling for less than you deserve. 4. Bank Mortgages Are Often More Restrictive Than You Think Not all mortgages are created equal. Some come with hidden traps—especially around penalties. Ever heard of a sky-high prepayment charge when someone breaks their mortgage early? That’s often due to something called an Interest Rate Differential (IRD) —and big banks are notorious for using the harshest IRD calculations. When we help you choose a mortgage, we don’t just focus on the interest rate. We look at the whole picture, including: Prepayment privileges Penalty calculations Portability Future flexibility That way, if your life changes, your mortgage won’t become a financial anchor. A Quick Recap What your bank typically offers: Only their own limited mortgage products Sales-focused representatives, not mortgage strategists Default rates that aren’t usually their best Restrictive contracts with high penalties What an independent mortgage professional delivers: Access to over 200 lenders and customized mortgage solutions Personalized advice and long-term financial strategy Competitive rates and terms upfront Transparent, flexible mortgage options designed around your needs Let’s Talk Before You Sign Your mortgage is likely the biggest financial commitment you’ll ever make. So why settle for a one-size-fits-all solution? If you're buying, refinancing, or renewing, I’d love to help you explore your options, explain the fine print, and find a mortgage that truly works for you. Let’s start with a conversation—no pressure, just good advice.

The Bank of Canada announced today that it is maintaining its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. For Canadian homeowners, buyers, and anyone with a mortgage on the horizon — here's what you need to know.

Owning a vacation home or an investment rental property is a dream for many Canadians. Whether it’s a cottage on the lake for family getaways or a rental unit to generate extra income, real estate can be both a lifestyle choice and a smart financial move. But before you dive in, it’s important to know what lenders look for when financing these types of properties. 1. Down Payment Requirements The biggest difference between buying a primary residence and a vacation or rental property is the down payment. Vacation property (owner-occupied, seasonal, or secondary home): Typically requires at least 5–10% down, depending on the lender and whether the property is winterized and accessible year-round. Rental property: Usually requires a minimum of 20% down. This is because rental income can fluctuate, and lenders want extra security before approving financing. 2. Property Type & Location Not all properties qualify for traditional mortgage financing. Lenders consider: Accessibility : Is the property accessible year-round (roads maintained, utilities available)? Condition : Seasonal or non-winterized cottages may not meet standard lending criteria. Zoning & Use : If it’s a rental, lenders want to ensure it complies with municipal bylaws and zoning regulations. Properties that fall outside these norms may require financing through alternative lenders, often with higher rates but more flexibility. 3. Rental Income Considerations If you’re buying a property with the intent to rent it out, lenders may factor the rental income into your mortgage application. Long-term rentals : Lenders typically accept 50–80% of the expected rental income when calculating your debt-service ratios. Short-term rentals (Airbnb, VRBO, etc.) : Many traditional lenders are cautious about using projected income from short-term rentals. Alternative lenders may be more flexible, depending on the property’s location and your financial profile. 4. Debt-Service Ratios Lenders use your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to determine if you can handle the mortgage payments alongside your other obligations. With investment or vacation properties, lenders may apply stricter guidelines, especially if your primary residence already carries a large mortgage. 5. Credit & Financial Stability Your credit score, employment history, and overall financial health still matter. Since vacation and rental properties are considered higher risk, lenders want reassurance that you can handle the additional debt—even if rental income fluctuates or the property sits vacant. 6. Insurance Requirements Rental properties often require specialized landlord insurance, and vacation homes may need coverage tailored to seasonal or secondary use. Lenders will want proof of adequate insurance before releasing mortgage funds. The Bottom Line Buying a vacation property or rental can be exciting, but financing these purchases comes with extra rules and considerations. From higher down payments to stricter property requirements, lenders want to be confident that you can handle the responsibility. If you’re considering a second property, the best step is to work with a mortgage professional who can compare lender requirements, outline your options, and find the financing that works best for you. Thinking about making your dream of a vacation or rental property a reality? Connect with us today.